If 2020 was distilled into a single theme it would be VUCA: Volatility, Uncertainty, Complexity, and Ambiguity. Investors have been trying to make sense of a world still grappling with the knock-on effects of a global pandemic that have had far reaching consequences – many yet to be calculated and realized. Add a contentious and polarizing U.S. presidential election and it raises a large yellow flag for investors to be cautious. Now, with less than a month to go until Election Day, the investment landscape looks more like a minefield than a runway. For many fixed income investors, the main concern right now is the economic impact of the election and its effect on portfolios.

As of October 7th, former V.P. Joe Biden is leading President Donald Trump in national polls, however, a few key swing states can easily turn the tide of the election outcome. Similar to the 2016 election, what happens in these crucial battleground states will ultimately determine which party has the power in Washington moving forward. Back on June 9th, Biden led Trump by eight percentage points in national polls, which is the largest lead by any presidential challenger since 1944, according to Real Clear Politics. Additionally, the majority of Senate seats up for reelection are held by incumbent Republicans, giving Democrats several opportunities to take control. That being said, 2016 has taught everyone a lesson that polls are not as reliable as once thought. Polls failed to accurately predict Trump’s election as well as a contentious Brexit vote across the Atlantic and as a result investors should remain skeptical of any polls’ predictive power and prepare for all potential outcomes.

How fixed income investors are positioning portfolios leading up to the election

Due to the ongoing coronavirus pandemic, millions of Americans will be voting via mail-in ballot and many anticipate election results will not be finalized for several days or weeks following the election. The easiest historical analogy for how investors may react in the case of drawn out results was the 2000 election when the recount and Supreme Court decision delayed a clear winner for six weeks following Election Day. There was an initial dip at first, with the Dow Jones industrial average falling 5% in the first two weeks as investors adjusted allocations to safer holdings, but the initial volatility didn’t last and investors went back to their long-term strategies. From discussions we’ve had with many fixed income managers, portfolios have generally been constructed with the long-term in mind and many uncertainties are already priced in at this point. Therefore, suggesting that any significant movements in positioning will be driven more by a perceived shift in longer-term fundamentals rather than initial shock should be viewed with some healthy skepticism.

Surprisingly, one of the scenarios that may have the most significant impact on bond markets is a clear and undisputed winner on November 3rd as it has the potential to push 10-year Treasury yields to 1% in the following weeks. Although this scenario is one of the most underappreciated risks, we discussed in our last case study that investors are focused on positioning their portfolios with an excess of cash to quickly take advantage of any opportunities that the election’s volatility may present through the end of 2020.

In the second blog in the election series, we discussed how there is more downside than upside over the next few weeks. A neutral portfolio is more likely to perform worse, which explains why fixed income investors are in a “risk-off” mode. Many portfolio managers are overweighting cash and credit quality, while underweighting duration, in order to take quick action after the election. That case study looked at how we would position a portfolio, particularly in the IG corporate space. In this case study, we expand into the muni market and explore sector under- and over-weights by taking into account all the volatility and uncertainty.

A muni portfolio case study: sector allocations vs. benchmark

The tax benefits that investors receive from munis is in itself a strong incentive for portfolios to hold municipal securities since an increase in taxes is part of the expected fall-out from COVID-19 over the next few years. Net fund flows have been strong this year, even after large outflows during March and April, and many fixed income portfolio managers believe that this trend will continue if Republicans retain control. If Democrats win, investors expect further fiscal stimulus, as well as fiscal support for municipalities. Even with a bullish sentiment, we are hearing that there are expectations for increased volatility in specific sectors, which is why an active approach to being overweight and underweight in specific sectors could have a significant impact to portfolios.

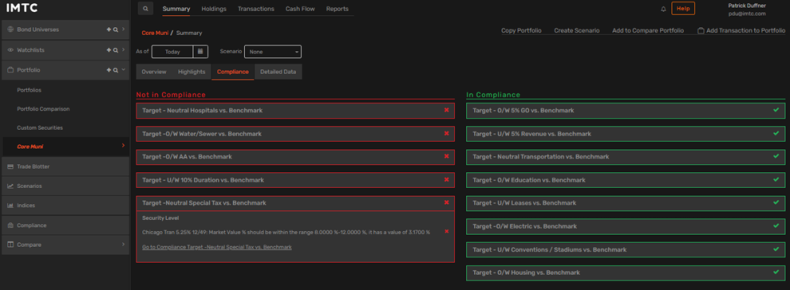

By taking an active management approach vs. the benchmark – in this case, Bloomberg Barclays 3-15 Year Blend Municipal Bond Index – it’s important to consider where you will overweight, underweight, or remain neutral.

Overweight vs. benchmark

- Water & Sewer – Expectations are for infrastructure spending to increase and water infrastructure bonds should perform well regardless of election results

- General Obligation – Higher quality states with fewer liabilities should provide stability during periods of volatility

- Electric – Infrastructure and increased electric usage are seen as credit positive

- Housing – If Democrats win, they could move to reverse the cap on state and local tax deductions, increasing the real estate value in higher tax states

Remain neutral vs. benchmark

- Transportation – Revenues are down on transportation bonds, but we see support through infrastructure spending

- Education – Colleges with larger endowments or school districts with growing population are stronger investment options

- Hospitals – Any healthcare legislation that increases the number of insured would be supportive of municipal healthcare issuers

- Special Tax – Analysis needs to be specific to underlying fundamentals

Underweight vs. benchmark

- Revenue – Target higher quality and avoid non-essential service revenue bonds

- Leases – Deteriorating credit quality of borrowers and limited demand makes leases riskier

- Assisted Living – Less demand will be a trend here and remains risky unless supplemental support, such as a county guarantee , is provided

- Conventions & Stadiums – No clear path to normalcy and depressed revenue in the medium-term for this sector

IMTC’s Investment Management System enables you to code your under- and over-weight exposures, highlighting where you need to add or trim your sector weights.

In the current VUCA environment, having a war chest of “dry powder” will minimize any near-term volatility and allow investors to redeploy their cash if and when any policy clarity presents new opportunities in the weeks following the election. For muni managers, considering specific sectors to overweight and which to underweight will be the biggest management strategy over the next month (or longer) until there is clarity on the election. The risks posed by the election as well as social, health, and geopolitical unknowns all factor into fixed income portfolio construction but the immediate impact has been relatively limited, and investors should remain opportunistic if they modeled their scenarios properly.

Technology is only as good as how it is used. IMTC is designed by and for fixed income professionals, empowering them to take action and make decisions quickly and accurately with real-time data and analytics capabilities. It allows you to future-proof your business; driving operational efficiencies, mitigating risk and delivering performance, to ultimately enable business growth. Learn more about IMTC.

This paper is intended for information and discussion purposes only. The information contained in this publication is derived from data obtained from sources believed by IMTC to be reliable and is given in good faith, but no guarantees are made by IMTC with regard to the accuracy, completeness, or suitability of the information presented. Nothing within this paper should be relied upon as investment advice, and nothing within shall confer rights or remedies upon, you or any of your employees, creditors, holders of securities or other equity holders or any other person. Any opinions expressed reflect the current judgment of the authors of this paper and do not necessarily represent the opinion of IMTC. IMTC expressly disclaims all representations and warranties, express, implied, statutory or otherwise, whatsoever, including, but not limited to: (i) warranties of merchantability, fitness for a particular purpose, suitability, usage, title, or noninfringement; (ii) that the contents of this white paper are free from error; and (iii) that such contents will not infringe third-party rights. The information contained within this paper is the intellectual property of IMTC and any further dissemination of this paper should attribute rights to IMTC and include this disclaimer.